Yesterday was a dark day in the Gendke household. The unexpected surprise of a $20,000 student loan bill all but put my husband into a depression. Understand: he’s not like me—he doesn’t get depressed easily. But if there’s one subject he’s touchy about, it’s money. Especially since we found out we’re having a baby, he’s been extra vigilant about cutting costs, paying off debt, and restructuring our finances.

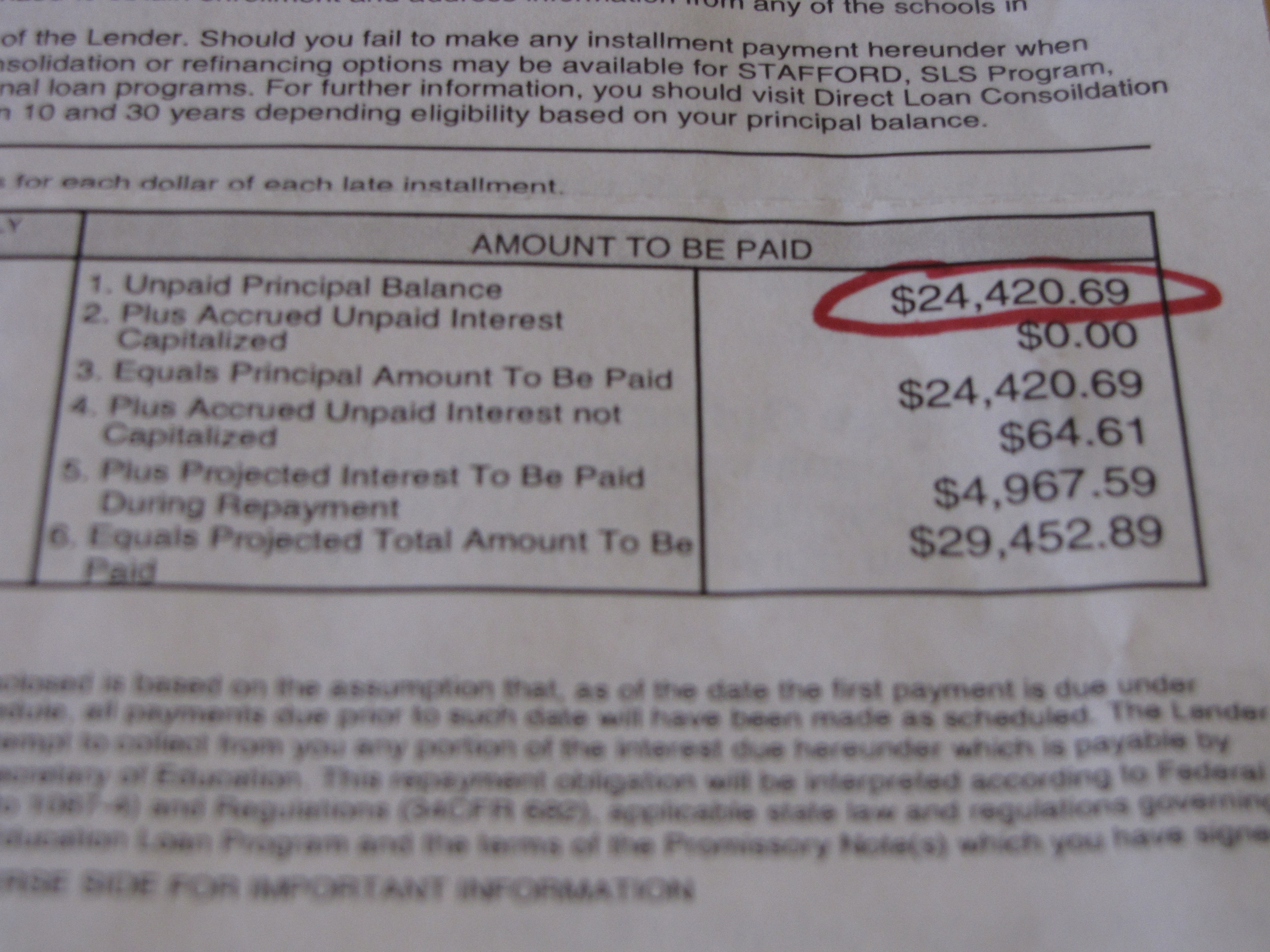

For two heady weeks, before we got the $20,000 note yesterday, he had it all planned out: pay off my $24,000 student loan (the old one—for my bachelor’s—but we made the mistake of thinking this included my master’s, too), then pay off his car, and finally, our home. By his calculations, he could have all this paid off by December, right before baby came.

Now, that won’t happen.

Don’t get me wrong. We’re hardly destitute or living month to month. My hubby’s investing skills and financial expertise have ensured abundance in eight years of marriage—still, we were so close to being out of debt.

For him, achieving financial freedom is about his number-one professional goal. And I love that about him—it makes me feel more secure—but sometimes that goal overshadows other areas of life. He’s not a worrier, but by golly, he does get so preoccupied about finances that he can be hard to talk to about anything else (to be fair, he’s often said the same about me and my writing).

His own family criticizes him for being “cheap”—for not always upgrading to the newest gadgets even though he could—and for giving our niece and nephew ten-year investment accounts, rather than cheap baubles for every birthday. However, what they don’t see is that these money-saving practices are what have allowed him to offer needy friends, family, and church members thousands and thousands (and thousands) of dollars of financial assistance over the years. They are also what will soon, perhaps within a few years, allow him to retire early and spend more than just nights and weekends with his family.

Call me cheap, too, but if you ask me, living frugally is just living smart. And for the comfortable, worry-free lifestyle my husband’s habits have offered me—a lifestyle better than I ever enjoyed before him—I am eternally grateful.

I just wish he didn’t worry so much.

I hate to see him, like I did yesterday, slumped over in his seat, head in hands, seeming bereft, as if all his dreams had been shattered. Worst of all, I hate feeling like I caused this.

Yesterday, seeing him like that I started to feel bad for getting my master’s degree, especially since now I’m not exactly “using” it. Of course, I feel I have used it in writing The Hidden Half of the Gospel—but when we’re talking about paying off a $20,000 bill, that book will only cover one-fourth to one-third of the cost.

I felt so bad I even apologized for being such an expensive wife (even if I don’t fit the usual profile of excessive shopper). All I could do to reassure him was to say, “Honey, look at all the good in our lives. Think of our wonderful marriage, and our baby coming. And even if you don’t see it right now, I do see benefit in the master’s because it gives me more and better job security if something should ever happen.”

He didn’t look convinced.

“Do you want me to look for a job now?” I tried next, clutching at straws.

He looked at me as if I were crazy.

“You’re pregnant. No.” Sigh. “Just keep doing what you’re doing. And write a bestseller.”

When I saw a wry smile playing at the corners of his lips, I sighed, too. With relief. I don’t want to take a typical job, not right now. But I think I would be willing to look if he wanted me to. At least, I hope I love him that much—as much as he obviously loves me.

Now, because of his pristine financial habits—and because he makes things sound worse than they are—I get to travel a mere ten feet to my work desk, and write about how we first met for my memoir—AKA my gestating bestseller:) Today, I’m sort of thankful, actually, that this little $20,000 “setback” has provided the perfect moment for me to remember exactly why I love this man.